The Construction industry depends on builders being able to make a profit, which then allows them to undertake further projects and continue to employ construction workers. Builders generally have to tender for new jobs. This means giving the customer a price and hoping to get the job. The builder usually has to compete with other builders who have also put in a price for the job.

Making a profit depends on accurately estimating the total cost of the job then adding the required amount of profit to arrive at the price. To accurately estimate a total cost you need to make sure every single item is included and correctly priced. You probably won’t need to price a large construction project for a while, however you’ll find that estimation and costing methods are much the same for all jobs.

In this chapter we will talk about:

Information you will need for estimation and costing can be obtained from:

When you have gathered your information, make sure you sort, file and record it in an orderly fashion so you can refer to it later.

Before leaving this page, think of what you've just been reading, and test yourself with these questions.

[[ mr /f ][ Which of these are likely to provide you with useful estimation and costing information? ][ Project plans. ][ Work specifications. ][ Worksite inspections. ][ Materials catalogues and pricelists. ][ * Prices of similarly finished products. ][ The finished price of a similar finished product will contain many hidden costs plus profit margins. ]]

Estimation is the process of working out quantities of materials and amounts of labour and time that will be needed to complete a job according to the plans and specifications.

When you estimate quantities it’s a good idea to work in the same sequence as when you construct the project. This way you are less likely to leave something out.

Remember it’s better to have a little material left over than to run short during the job. Running out of material causes time delays which are usually more costly than having a small amount of material left over.

Depending on the type of material, you can estimate quantities as:

Calculations

Basic calculations for these measures are covered in the chapter on Measurements & Calculations so we won’t repeat them here. However, it is very important that you understand these calculations before you attempt to do an estimate for your construction project. Go back now and revise any calculations you are not sure of.

Here we will simply summarise what you need to know about estimating quantities for some common building materials.

Brickwork

Bricks are calculated by the square metre (m2) then converted to thousands, usually rounding up to the next 1000 for larger jobs. There are approximately 50 bricks to the square metre. Depending on the size of the job and the amount of cutting, a waste allowance of 5% or more can be added.

Mortar: Sand is bought by the cubic metre (m3). For mortar in general brickwork 0·6m3 of sand is required for each 1000 bricks to be laid. Cement is bought by the tonne for large jobs. There are 25 x 40kg bags to the tonne. An average mortar mix will require about 5 bags of cement per 1000 bricks.

Concrete

Concrete is calculated in cubic metres (m3). Where the concrete is to be poured on the ground 10% is added for waste and discrepancies and 5% where the concrete is poured into formwork.

Pre-mixed concrete suppliers usually have a minimum quantity they will deliver. Make sure you check this with your supplier if you are taking off quantities for a small job.

Site mixed concrete (4:2:1 mix) takes about 1·6m3 of dry ingredients to make 1m3of wet concrete. For each cubic metre of concrete you can allow approximately 0·9m3 of coarse aggregate, 0·45m3 of sand and 8.5 bags of cement. Don’t forget to add the allowance for waste and discrepancies.

Timber

Mouldings such as architraves, skirtings and quad as well as stops and jambs for window and door openings are calculated in the lengths required for the job but costed per linear metre or sometimes per hundred linear metres.

House framing is calculated in lengths required and costed per linear metre or per cubic metre (m3) for larger quantities. Standard framing members such as studs are sometimes priced per piece.

Sheet Materials

Sheet materials such as plasterboard, particleboard flooring, plywood and fibre cement are calculated in the sheet sizes to suit the job and priced per square metre with allowances as required.

In practice, allowances are usually made only for large openings. Depending on the job a cutting allowance of up to 10% could be necessary.

Paint

The number of litres of paint required is found by dividing the area to be covered by the coverage rate. Area is calculated in square metres (m2) and the coverage per litre is given on the can or drum. Coverage per litre can vary with the type of paint and allowance may have to be made for porous surfaces.

Unfortunately there’s no magic formula for estimating the number of construction workers that will be needed or the time they will take to do a job. These estimates are generally based on past experience. In other words, you look at the records of past jobs and go from there.

An Example

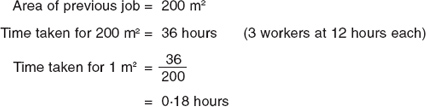

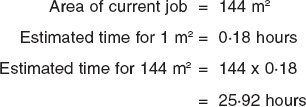

You need to estimate labour and time to prepare the ground, erect formwork and install reinforcing for a 150mm concrete driveway that will have a surface area of 144m2. Look through pages 194 to 199 to see what you’d have to do to ‘form and prep’ a concrete job. ‘Form and prep’ is a construction industry term for this task.

On one of your other jobs it took 3 construction workers 12 hours to form and prep a 150mm driveway with a surface area of 200m2. From past experience you know 3 workers will be needed to set up the long forms and handle the reinforcing steel, but how long will it take?

A common method is to work out a unit rate that you can use to estimate time for any similar job. In this case you could work out how long it would take for each square metre of surface area.

Now that you have your unit rate you can use it to estimate the time for any similar 150mm concreting job.

Round up your estimate to the next whole hour for each worker. You can allow 9 hours for each of 3 workers giving a total of 27 labour hours. Remember it’s always better to allow a little extra than not enough.

Unit Rates

A unit rate can be calculated for most construction tasks. The unit of measurement will depend on the nature of the task. For example, an estimate for assembling and standing wall frames could be based on time taken per linear metre of frame.

You could calculate the unit rate from the total linear metres of framing in a past job and the total time it took to assemble and stand the frames.

The linear metres of framing would be taken off the floor plan for the job and time would come from the carpenters’ time sheets. Once again, when you have calculated your unit rate you can use it to estimate time for any similar job.

Before leaving this page, think of what you've just been reading, and test yourself with these questions.

[[ mm /f ][ Match the materials mentioned to the the typical quantity required: ][ Number of standard bricks to the square metre: ~ 50 ][ Volume of sand (in m3) for mortar per 1000 bricks laid: ~ 0.6 ][ Bags of cement for mortar per 1000 bricks: ~ 5 ][ Waste allowance (as a %) for concrete poured on the ground: ~ 10 ][ Number of bags of cement to the tonne: ~ 25 ][ Number of bricks = 50; Volume of sand for mortar = 0.6; Bags of cement for mortar = 5; Waste for concrete poured on the ground = 10; Number of bags = 25. ]]

[[mc /f ][ Which of the following isn't a primary consideration in the estimation of quantities? ][ * Ensuring sufficient materials. ][ * Estimating by following the work flow. ][ * Ensuring sufficient labour. ][ Calculating the total cost of the job. ][ * Estimating the project time scale. ][ Total cost calculations are secondary to estimating the quantities of materials, labour and time needed for th project. ]]

[[ mr /f ][ You've got to mix about 1.5m3 of concrete on site, including an allowance for waste. How much of the dry ingredients do you need? ][ 13 bags of cement. ][ * 15 bags of cement. ][ 1.4m3 of aggregate. ][ * 1.5m3 of aggregate. ][ 0.7m3 of sand. ][ * 1.5m3 of sand. ][ For this amount of concrete, 13 bags of cement, 1.4m3 of aggregate and 0.7m3 of sand is sufficient. ]]

There are many different ways of breaking down costs and arriving at a final price for a construction job. Some builders use a computer program such as Buildsoft which works out the cost when quantities and rates are entered into a template.

Costing a project should include actual job costs plus an allowance for the cost of doing business. These extra costs are called overheads. Costing a project is usually broken down into preliminaries, materials, labour, overheads and mark-up.

‘Preliminaries’ is a term often used to describe site costs that are not material or labour costs. Preliminaries include costs such as site office, professional fees; hire of equipment, scaffold or work platforms, temporary toilet, skip; temporary power supply, clean-up, etc. Preliminaries are charged as applicable. Some might be a one-off charge while others might be charged at a given rate such as weekly hire.

When material quantities have been taken off as single items, square metres, cubic metres etc, they are then costed by multiplying the quantity by the cost per unit. For example 120m x $3·50 per metre = $420.

Labour is charged out at an hourly rate according to the worker’s qualifications or classification. For example, 27 hours labour at $34·67 per hour = $936. The charge out rate for labour usually includes an allowance for other labour costs such as holiday pay, sick pay and long service leave.

Overheads consist of costs such as administration and office expenses, insurance, vehicle expenses, travelling, office staff, etc. These are the costs of running the business and are shared out over all the jobs during the year.

An allowance for overheads is usually included in the cost of a job as a percentage of all other costs. If the overhead rate is, say, 5%, the actual job cost could be multiplied by 1·05 to include overheads. For example $175,000 x 1.05 = $183,750.

The mark-up or profit margin is an amount the builder needs to make, over and above all costs. This is usually worked out as a percentage of total costs, generally in the range from 5% to 10%. It is common practice for estimators to include a combined amount for mark-up and overheads usually in the range from 8% to 15% depending on the size of the job.

Unit rates can be used in costing as well as for estimating quantities. For many items a single rate can be used for quantity and cost. In the example on page 212, the job takes 0·18 hours for every square metre.

Using the charge out rate of $34.67 per hour as in ‘Labour’ above, 0·18 hours of labour costs $6.24, ($34·67 x 0·18 = $6·24). This means that the labour cost to form and prep each square metre of the job is $6·24.

The example on page 212 shows the estimated total time for the job is 25·92 hours, therefore the estimated cost is $899, (25·92 x $34·67 = $899 to the nearest $). The same figure could have been found by multiplying the number of square metres by the rate, (144 x $6·24 = $899).

Before leaving this page, think of what you've just been reading, and test yourself with these questions.

[[ mr /f ][ Which of these should be costed as "preliminaries"? ][ Hire of temporary fencing. ][ Hire of scaffolding. ][ Delivery and removal of skip. ][ Security camera installation. ][ * labour for site works. ][ Labour isn't paid for until the job begins. ]]

[[ mr /f ][ Which of the following would be included in "overheads"? ][ Wages for office staff. ][ Insurance. ][ Security contractors. ][ * Apprentices wages. ][ * Sub-contractors wages. ][ Wages are actual work costs, rather than overheads. ]]

You need to accurately record all costing details so you can double check the figures and make sure you have left nothing out. It is also very important to keep accurate records for future reference. Remember, unit rates are generally calculated from the records of past jobs.

The previous examples showed how to work out rates for time per square metre and also labour cost per square metre for the concrete driveway.

In practice you would probably use an overall rate per square metre to estimate the total cost. This rate would include all material, labour and other job costs.

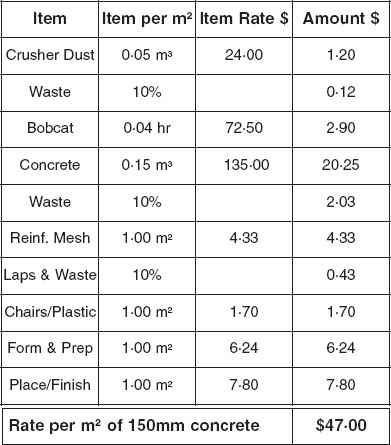

The table on the right shows a typical way to document costing.

The Amount column shows the cost per square metre of each item. The total at the bottom is the cost or rate per square metre of finished concrete. The cost of the concrete driveway in our example is found by multiplying the number of square metres by the rate per square metre, (144 x $47 = $6,768).

You can calculate rates in much the same way for different parts of the project. For example, you could calculate a rate per linear metre for footings, per square metre for the floor slab, per linear metre for the framing and so on. You need to update rates whenever material prices, wage costs or construction methods change.

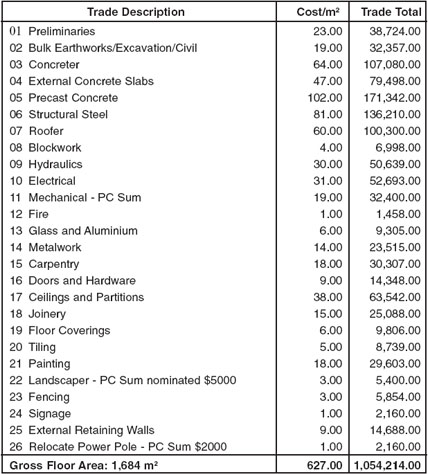

An estimate summary brings together all the different cost items to arrive at a total. Mark-up and overhead percentages are applied to the total cost to give the final price for the job. The example below is an estimate summary for the first of several buildings to be constructed on an industrial estate.

Note that the item costs have been brought down to a cost per square metre of gross floor area rounded to the nearest dollar. The overall cost per square metre is $627. These figures can be used when costing similar buildings or to compare estimates for similar buildings. Note also that a number of the cost items in the summary would be quotes from subcontractors.

The final price of the job is found by applying mark-up and overhead rates to the total cost as shown in the table.

It is very important that you check and double check all calculations and estimates. Any items you leave out or calculate wrongly will mean less profit or the job could even lose money.

If possible, get someone else to verify your estimates. If that’s not possible try using a different method to check your original estimates. For example, if you used a square metre rate for an estimate, check your figures by costing material quantities and labour separately.

You should keep all costing documents and calculations for future reference. Remember, the best way to estimate labour and time is to use information from past jobs. If you haven’t got records of past jobs to go by, you’ll have to give it your best guess. A guess is still a guess, even if it is based on experience.

If you use a computer program for estimating, make sure you save all documents and keep a backup copy. Be careful to enter quantities and costs accurately. You have probably heard the old computer saying ‘garbage in, garbage out’.

Before leaving this page, think of what you've just been reading, and test yourself with these questions.

[[ mc /f ][ Why does a job estimate summary give a cost per square metre figure? ][ This is useful for comparing estimates with similar buildings / types. ][ * This is a good way to verify your estimate. ][ * It lets you see if the estimate is reasonable. ][ * It lets you see if you missed anything in the estimate. ][ This figure lets you compare estimates between buildings of different sizes but similar types. ]]